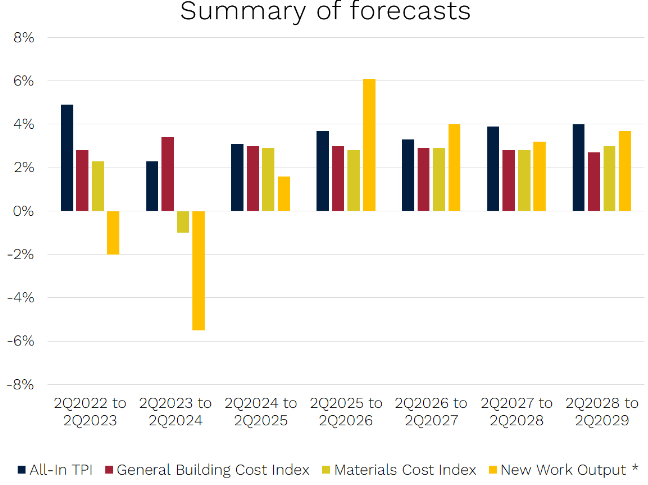

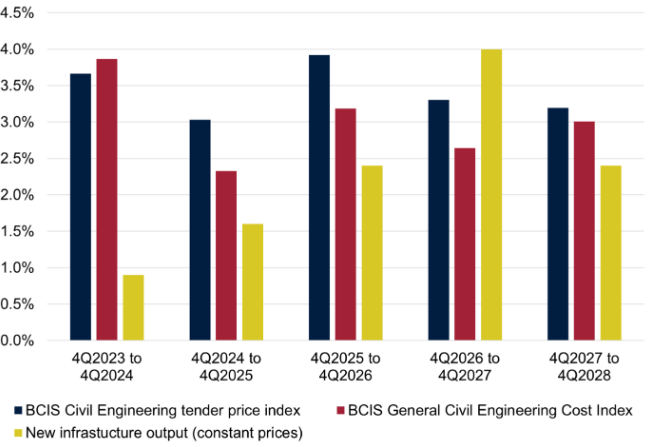

BCIS Construction and Infrastructure Forecast: 2024-2029

Source: bcis.co.uk

Want to read more like this story?

The Price of Progress: Why UK Infrastructure Costs Need Reform

Oct, 10, 2024 | NewsThe rising costs of infrastructure projects in the UK have been a significant concern for decades,...

Construction material costs resume upward climb as copper and concrete pressure builds into 2026

Jan, 29, 2026 | NewsAfter nearly three years of relative stability, construction material costs are once again trending...

London: The World’s Most Expensive City for Construction in 2024

Apr, 16, 2024 | NewsLondon has emerged as the most expensive city for construction in 2024, narrowly edging out Genev...

2024’s Construction Boom: What It Means for 2025 and Beyond

Nov, 29, 2024 | NewsThe construction industry in 2024 demonstrated resilience and growth, marked by a 10% increase in n...

Record Growth in UK Construction: Civil Engineering Leads the Way

Aug, 07, 2024 | NewsSurge in Construction Activity The UK construction sector has experienced its fastest growth in ov...

Offshore wind sector costs could be reduced by 40% in 10 years’ time according to new Dutch research

Jun, 29, 2016 | NewsThe key is the cooperation between industry, knowledge institutes and government The key is...

Forecast that construction market will reach $13 trillion by 2022

Nov, 01, 2018 | NewsA research by GlobalData suggests that the international construction market output will hit ab...

World's most expensive places to build

Sep, 03, 2018 | NewsNew research by Turner & Townsend has revealed the world's most expensive places to build....

Data-Driven Construction: The Key to Meeting Global Infrastructure Demands

Feb, 14, 2025 | NewsAs the global population is set to reach 9.7 billion by 2050, the demand for new and upgraded infra...

Trending

Taipei 101’s impressive tuned mass damper

Characteristics of Load Bearing Masonry Construction

Understanding the Carola Bridge Collapse: Expert Insights

This powder offers an innovative solution to water purification

Dutch greenhouses have revolutionized modern farming

Formwork failure causes roof slab collapse in Limassol construction site